You’ve been saving, scrolling through listings, and wondering if homeownership is really possible in 2026 — especially with current mortgage rates and home prices.

Here’s the truth: you don’t need perfect credit or 20% down to buy your first home.

At Martini Mortgage Group, we specialize in helping North Carolina homebuyers unlock the power of the FHA Loan Raleigh NC program — one of the most flexible, affordable mortgage options available today.

Led by Certified Mortgage Advisor Kevin Martini and Raleigh Mortgage Broker Logan Martini, our fiduciary-style approach prioritizes your long-term financial strategy over the loan itself. We call it clarity-based lending because when you understand your options, you can make decisions with confidence.

Complete FHA Loan Raleigh NC Guide: Topics Covered

Why FHA Loans Still Make Sense for Raleigh Buyers in 2026

The FHA Loan Raleigh NC program, backed by the Federal Housing Administration, was designed to help more Americans become homeowners — and it remains one of the most trusted financing options for Raleigh buyers seeking stability, predictability, and low down payments.

Here’s why FHA loans continue to be a powerful option in today’s market:

✅ Low Down Payment – You can buy with as little as 3.5% down, keeping more cash for moving expenses or emergency savings.

✅ Flexible Credit Requirements – Many FHA homebuyers qualify with credit scores starting at 580 — and sometimes even lower with compensating factors.

✅ Competitive Interest Rates – FHA loans often feature lower rates than conventional mortgages, which can translate to a more affordable monthly payment.

✅ Gift Funds Allowed – Your down payment can come from family, friends, or even an employer — helping you get started sooner.

✅ Assumable Mortgages – Future buyers can assume your FHA loan’s low rate, making your home even more valuable if rates rise.

In a market where rents are climbing and savings are tight, FHA financing gives Raleigh buyers a way to stop renting and start building real equity — one payment at a time.

What Homebuyers (First-Time and Repeat) Need to Know About FHA Down Payments

Many people think FHA loans are only for first-time homebuyers — but that’s a myth.

The FHA Home Loan is open to any eligible buyer, whether you’re purchasing your very first home or your fifth. The key is that the home must be your primary residence.

Here’s what makes the FHA loan such a powerful (and flexible) mortgage solution:

- Not Just for First-Timers: Repeat homebuyers can use an FHA loan, even if they’ve owned a home before — there’s no “first-time buyer only” restriction.

- You Can Use It Again: If you’ve had an FHA loan in the past and sold that property, you’re still eligible to use the program again.

- Yes, Two FHA Loans Are Possible: In very specific circumstances — such as a job relocation, divorce, or family size change — FHA guidelines may allow you to hold two FHA loans at once. (This requires meeting certain occupancy and distance rules.)

- Low Down Payments Still Apply: Whether you’re a first-time or repeat buyer, an FHA Loan Raleigh NC still allows you to qualify with as little as 3.5% down, provided you meet credit and income guidelines.

This flexibility is one of the reasons FHA loans remain one of the most trusted tools for Raleigh homebuyers.

At Martini Mortgage Group, we help both first-time and repeat buyers strategically use the FHA loan to build long-term wealth — whether it’s your starter home, your move-up home, or your next chapter.

(You can explore all your options in our North Carolina Mortgage Guide).

The Fiduciary Difference: Why Raleigh Chooses Martini Mortgage Group

At Martini Mortgage Group, we don’t sell loans — we design strategies.

Our fiduciary-style approach means your goals always come first. Instead of steering you toward one lender’s products, we evaluate multiple options to find the structure that fits your life, your timeline, and your wealth-building goals.

Here’s what that looks like in practice:

✨ Same-As-Cash Approval — Our clients’ offers stand out because they carry the strength of cash. Sellers notice. You gain leverage. No surprises, no delays.

✨ Mortgages Under Management — After closing, our relationship continues. We proactively monitor your mortgage and reach out when the market shifts — so you never miss a chance to save.

✨ Transparent, Stress-Free Process — From application to keys in hand, we simplify every step, giving you the clarity, certainty, and confidence to move forward.

When you work with Kevin Martini or Logan Martini, you’re not just getting a mortgage — you’re gaining a long-term fiduciary partner who ensures your FHA Loan Raleigh NC strategy aligns with your broader wealth goals.

FHA vs. Conventional Loans: Which Is Right for You?

Both FHA and conventional loans have unique benefits. The right one depends on your credit, income, and long-term goals.

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Down Payment | 3.5% | 3% (with stricter guidelines) |

| Credit Flexibility | More forgiving | Requires higher credit scores |

| Mortgage Insurance | Required for all | Can be removed after 20% equity |

| Loan Limits (Raleigh 2026) | $541,287 | $832,750 (conforming) |

| Ideal For | First-time buyers, repeat homebuyers, lower credit | Strong credit, larger down payment |

At Martini Mortgage Group, we’ll help you evaluate both — so you can choose the path that builds maximum wealth with minimum stress.

FHA Loan Limits in Raleigh and the Triangle of North Carolina for 2026

Every year, the Federal Housing Administration (FHA) updates its loan limits to reflect changes in home prices. For 2026, FHA loan limits have increased across much of North Carolina — giving buyers greater purchasing power.

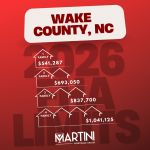

2026 FHA Loan Limits (Wake County)

1-Unit (Single-Family Home): $541,287

2-Unit Property: $693,050

3-Unit Property: $837,700

4-Unit Property: $1,041,125

2025 FHA Loan Limits (Johnston County)

1-Unit (Single-Family Home): $541,287

2-Unit Property: $693,050

3-Unit Property: $837,700

4-Unit Property: $1,041,125

2025 FHA Loan Limits (Durham County)

1-Unit (Single-Family Home): $634,800

2-Unit Property: $812,650

3-Unit Property: $982,300

4-Unit Property: $1,220,800

100% Financing: Martini Mortgage Group’s No-Down-Payment FHA Home Loan

For many Raleigh and North Carolina homebuyers, the biggest barrier to homeownership isn’t credit — it’s cash. That’s why Martini Mortgage Group developed a proprietary FHA Loan Raleigh NC no-down-payment program, designed to make homeownership more accessible without sacrificing financial stability.

This program combines the flexibility of a standard FHA-insured mortgage with a second loan or grant that covers your required 3.5% down payment — allowing qualified borrowers to achieve 100% financing.

How the Program Works

Here’s how our no-down-payment FHA structure removes one of the biggest financial hurdles:

- Two-Loan Structure: You receive a traditional FHA first mortgage, paired with a second loan or grant that covers the 3.5% FHA down payment requirement.

- Two Types of Assistance:

- Repayable Option: A low-interest second mortgage with manageable monthly payments.

- Forgivable Option: A 0%-interest second mortgage that may be forgiven entirely after you’ve lived in the home for a set period (typically 5–10 years).

- Increased Accessibility: By covering the down payment, this program empowers eligible buyers to purchase a home sooner — while still benefiting from FHA’s flexible credit and debt-to-income standards.

This means more Raleigh families can stop renting and start building equity — even if saving for a down payment has felt out of reach.

Who Qualifies for Martini Mortgage Group’s No-Down-Payment FHA Program

Eligibility for this program depends on both FHA requirements and guidelines from Martini Mortgage Group’s down-payment-assistance partners. Common qualifications include:

✅ Meeting standard FHA loan eligibility (credit, income, and primary-residence requirements).

✅ Available to both first-time and repeat homebuyers — no three-year lookback is required.

✅ Completing a homebuyer education course to ensure confidence and understanding before closing.

✅ Holding a credit score of 600 or higher, though exceptions may apply.

NOTE: $0 down payment doesn’t mean $0 due at closing—closing costs still apply (can be covered via seller credits or gift funds, when available).

Why This Program Matters

This innovative approach bridges the gap between affordability and opportunity. It’s not just about buying a home — it’s about giving qualified families the chance to build generational wealth sooner.

At Martini Mortgage Group, we believe homeownership shouldn’t be defined by how much cash you have saved — but by how ready you are to invest in your future.

If you’re in Raleigh or anywhere in North Carolina and want to explore 100% FHA financing, our team is ready to guide you through every step with clarity and confidence.

Transform a Fixer-Upper into Your Dream Home with the FHA 203(k) Limited Loan

Sometimes the right home isn’t perfect — yet.

If you’ve found a property in Raleigh, or anywhere in North Carolina, that needs a little love, the FHA Loan Raleigh NC 203(k) Limited option can help you finance both the purchase and renovation with one mortgage

How the FHA 203(k) Limited Loan Works

This program combines an FHA-insured first mortgage with built-in renovation funds, allowing you to update, repair, or improve your home immediately after closing — without needing separate financing.

Common eligible projects include:

- Kitchen or bathroom updates (fixtures, cabinets)

- Interior or exterior painting

- Roof repair (non-structural)

- HVAC replacement

- Floor upgrades (hardwood, tile, carpet)

- Window or door replacements

- Minor electrical or plumbing repairs

- Energy-efficiency improvements

Up to $75,000 in renovation costs can be financed directly into your mortgage — meaning one loan, one payment, and one simple process.

Why Raleigh Buyers Choose the 203(k) Limited Loan

✅ Buy the right home, not just the right now home. You can look beyond move-in-ready listings and focus on neighborhoods or homes with untapped value.

✅ Increase equity from day one. Strategic updates often boost a property’s market value faster than standard appreciation alone.

✅ Streamlined process. The “Limited” version of the 203(k) avoids the complexity of the full 203(k) Standard loan, making it faster and easier to close.

(You can explore all your options in our FHA 203(k) Limited Loan: The Smart Way to Buy a Fixer-Upper in Raleigh).

How to Get Pre-Approved for an FHA Loan in Raleigh

Getting started with an FHA Loan Raleigh, NC, through Martini Mortgage Group is simple, transparent, and empowering.

Step 1: Schedule a Complimentary Consultation

→ Book your free call today with Kevin Martini or Logan Martini.

Step 2: Know Your Numbers

We’ll walk you through your credit, income, and down payment options — turning confusing terms into clear next steps.

Step 3: Get Same-As-Cash Approval

Strengthen your offer with an approval that gives you the leverage of a cash buyer.

Step 4: Shop with Confidence

Work with your Realtor knowing exactly what you can afford — no guesswork, no surprises.

Step 5: Close with Certainty

Our team coordinates every detail for a smooth, on-time closing — and we’ll keep managing your mortgage long after.

The Bottom Line: Clarity Creates Confidence

Homeownership isn’t about timing the market — it’s about having a strategy that works in any market.

An FHA Loan Raleigh NC remains one of the most effective ways for North Carolina families to achieve affordable homeownership — especially when paired with strategic mortgage planning.

When you’re ready to stop renting and start building wealth, let’s talk.

👉 Schedule your complimentary consultation and take your first confident step toward homeownership today.

Clarity = Certainty. Certainty = Power.

If you’re ready to explore your options with a fiduciary-style FHA Loan Raleigh NC partner, schedule your complimentary consultation today with Kevin or Logan Martini.

NOTE: The Martini Mortgage Group isn’t merely a Raleigh Mortgage Broker in Raleigh, North Carolina. Their reach spans across all 100 counties in North Carolina. It extends into Florida, Georgia, Indiana, South Carolina, and Virginia, serving individuals and families alike

2026 FHA Loan Limits in Raleigh & Wake County: FAQs for Homebuyers

What is the FHA loan limit in Raleigh, NC for 2026?

The FHA loan limit in Raleigh, North Carolina for 2026 is the same as the Wake County limit and is set by the U.S. Department of Housing and Urban Development (HUD).

For 2026, the FHA loan limits in Raleigh/Wake County are:

$541,287 for single-family homes

$693,050 for duplexes

$837,700 for triplexes

$1,041,125 for quadplexes

These limits apply to FHA-eligible primary residences located in Raleigh and throughout Wake County.

What is the FHA loan limit in Wake County, NC for 2026?

The FHA loan limit in Wake County for 2026 represents the maximum FHA-insured loan amount allowed by HUD for properties in the county.

For 2026, the FHA loan limits in Wake County are:

$541,287 for single-family homes

$693,050 for duplexes

$837,700 for triplexes

$1,041,125 for quadplexes

These limits apply to all cities within Wake County, including Raleigh, Cary, Apex, Wake Forest, and Fuquay-Varina.

What is the 2026 FHA loan limit in Johnston County, North Carolina?

The FHA loan limit in Johnston County for 2026 represents the maximum FHA-insured loan amount allowed by HUD for properties in the county.

For 2026, the FHA loan limits in Wake County are:

$541,287 for single-family homes

$693,050 for duplexes

$837,700 for triplexes

$1,041,125 for quadplexes

These limits apply to FHA-eligible primary residences located throughout Johnston County.

Can repeat buyers or existing homeowners use FHA loans up to the 2026 limit?

Yes. FHA loans are not limited to first-time buyers.

Repeat buyers and existing homeowners may qualify for FHA financing up to the 2026 loan limit, provided the property is used as a primary residence, and the FHA guidelines are met.

For 2026, the FHA loan limit for a single-family home in Wake County, NC is $541,287.

Is the FHA loan limit the same across all of North Carolina?

No. FHA loan limits vary by county across North Carolina.

HUD sets FHA loan limits annually based on local median home prices. Counties with higher home values generally have higher FHA loan limits, while lower-cost counties have lower limits.

Kevin Martini

Logan Martini