For perspective, basically a year ago, Raleigh mortgage rates started with a 3 and now they start with a 7. The last time Raleigh mortgage rates were at this level was in Spring 2002 and that was 20-years ago! Many experts predict, Raleigh mortgage rates will starts with an 8 sooner than we will see home loan rates that starts with a 5.

The Fed’s past, and likely future, tightening actions are engineered to decrease demand in order to reduce inflation. The Fed’s action are working as it relates to the housing and mortgage markets market.

The Free Martini Mortgage Group at Gold Star Mortgage Buydown Calculator

Increasing Raleigh mortgage rates are presenting some challenges and opportunities not just to first-time homebuyers but also to repeat homebuyers too!

Raleigh Homebuyer Opportunity

Raleigh mortgage rates are not the only thing going up, rents are too! Sure, we are seeing a deceleration of appreciation and it is possible to see a month-over-month decline of home values however annual home values are not forecasted to decline since there remains a supply and demand imbalance with real estate that could take a decade to resolve.

In this market, buyers are finding unprecedented homeownership opportunities.

Logan Martini | Raleigh Mortgage Broker with Martini Mortgage Group

Raleigh Homebuyer Challenge

It’s just a fact! The sharp upward movement in home loan rates is making home buying more challenging. Affordability and buying power is impacted in the current environment. With elevated home loan rates impact home affordability. When home loan rates move upwards by 1%, buying power is reduced by 10%.

Kevin Martini | Raleigh Mortgage Broker with Martini Mortgage Group

Buydown Home Loan Programs | a Martini Mortgage Group creative strategy to help Raleigh homebuyers to leap over the challenges and take advantage of the Raleigh real estate opportunity to become a homeowners.

What is the Martini Mortgage Group buydown loan program (a.k.a. Seller-Paid Buydown)?

The Martini Mortgage Group Buydown Program offered by Logan Martini and Kevin Martini is where where the seller pays a fee at the closing to reduce the interest rate on the buyer’s mortgage temporarily. This results in temporarily lowering the buyer’s monthly cost and making the home more affordable for a homebuyer today.

A buydown reduces the homebuyer’s interest rate and monthly cost during the first few years(s) of homeownership, making the home more affordable for homebuyers. It has a much greater impact on the homebuyer’s monthly payment than reducing the list price of the home.

The Martini Mortgage Group, a Raleigh mortgage lender, Buydown Program has three options (i.e. 1-0 Buydown, 2-1 Buydown & 3-2-1 Buydown).

1-0 Buydown

Seller pays a fee at closing (the fee must be within the Interested Parties Contribution based on the loan the homebuyer is securing) to reduce the interest rate on the Raleigh homebuyer’s mortgage by 1% in year 1.

an example of the 1-0 buydown Program by Martini Mortgage Group, a Raleigh mortgage lender

For illustration ONLY: if homebuyer purchased $400,000 home and put 20% down with a 30-year fixed rate of 7%, they would have a P&I payment of $2,129. However, if the homebuyer requested (or the seller offered) at list price (e.g. $400,000) the Martini Mortgage Group 1-0 Buydown Program, the rate would be reduced by 1% for the first year (i.e. 6% in this example for illustration ONLY). The homebuyer would save $2,520 of P&I during the first year and that is a savings of $210 a month to the homebuyer.

2-1 Buydown

Seller pays a fee at closing (the fee must be within the Interested Parties Contribution based on the loan the homebuyer is securing) reduce the interest rates on the buyer’s mortgage by 2% in year 1 and 1% in year 2.

an example of the 2-1 buydown Program by Martini Mortgage Group, a Raleigh mortgage lender

For illustration ONLY: if homebuyer purchased $400,000 home and put 20% down with a 30-year fixed rate of 7%, they would have a P&I payment of $2,129. However, if the homebuyer requested (or the seller offered) at list price (e.g. $400,000) the Martini Mortgage Group 2-1 Buydown Program, the interest rate would be reduced by 2% for the first year (i.e. 5% in this example for illustration ONLY).

During the first year of the 2-1 Martini Mortgage Group Buydown Program, the homebuyer would save $4,932 of P&I. That is a savings of $411 a month to the homebuyer during the first year.

During the second year of the 2-1 Martini Mortgage Group Buydown Program, the homebuyer would save $2,520 of P&I. That is a savings of $210 a month to the homebuyer during the second year.

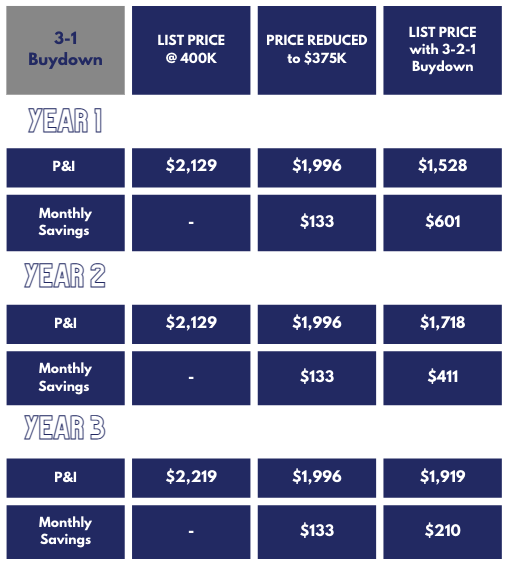

3-2-1 Buydown

Seller pays a fee at closing (the fee must be within the Interested Parties Contribution based on the loan the homebuyer is securing) reduce the interest rates on the Raleigh homebuyer’s mortgage by 3% in year 1, 2% in year 2 and 1% in year 3.

an example of the 3-2-1 buydown Program by Martini Mortgage Group, a Raleigh mortgage lender

For illustration ONLY: if homebuyer purchased $400,000 home and put 20% down with a 30-year fixed rate of 7%, they would have a P&I payment of $2,129. However, if the homebuyer requested (or the seller offered) at list price (e.g. $400,000) the Martini Mortgage Group 3-2-1 Buydown Program, the rate would be reduced by 3% for the first year (i.e. 4% in this example for illustration ONLY).

During the first year of the 3-2-1 Martini Mortgage Group Buydown Program, the homebuyer would save $7,212 of P&I. That is a savings of $601 a month to the homebuyer during the first year.

During the second year of the 3-2-1 Martini Mortgage Group Buydown Program, the homebuyer would save $4,932 of P&I. That is a savings of $411 a month to the homebuyer during the second year.

During the third year of the 3-2-1 Martini Mortgage Group Buydown Program, the homebuyer would save $2,520 of P&I. That is a savings of $210 a month to the homebuyer during the third year.

Raleigh Homebuyers Consider Martini Mortgage Group Buydown Home Loan Program A Quasi Asset

At time of sale or refinance, the unused balance of the buydown is credited to the customer.

Is the Martini Buydown Program the Best Mortgage Loan Program if securing a home loan in Raleigh, North Carolina for a first-time or repeat homebuyer?

It depends! Sadly no mortgage company website can determine the clients best loan options. Obviously payments are more affordable temporarily not permanently with a buydown home loan program so, a customer needs to consider the length of time they will be in the home loan to determine the true benefit.

Since many industry experts and Fannie Mae are predicting a conventional interest rates will start with a 4 in late 2023 or early 2024, it is likely the loan program a customer gets today they will likely be refinancing in 12- to 18 months.

I have been in the financial services since the late 80’s and exclusively in the mortgage industry since 2006 in Raleigh, North Carolina. I have yet to meet two clients that have the same financial needs.

A home loan solution for a home purchase may be different than one that is for a refinance. Perhaps a FHA home loan is the proper home loan financing solution for a customer to buy a home with but a conventional is the proper lending solution to when refinancing.

Whether buying a home in Raleigh, NC or refinancing a mortgage, a customer needs to understand it is a process not an event to secure the proper home loan financing solution. The process does not need to be painful, it should be free and educational while providing the customer with price and cost clarity with certainty.

Kevin Martini | Raleigh Mortgage Broker with Martini Mortgage Group

Advantages AND disadvantages of Buydown loan options

With anything, when there are advantages, there are likely disadvantages and this sentiment is true with buydowns. Things to consider are: the prevailing rate, the amount of the loan, the amount of interest saved, how loan you are expecting to be in the loan and your future income.

Advantages of Buydown loan options

- a temporary reduction of interest rate provides payment assistance to Raleigh homebuyers

- the potential opportunity to purchase a home in Raleigh, North Carolina less than list price

- the ability for a first time or repeat homebuyer to ease into a payment

disadvantages of Buydown loan options

- once the temporary reduction of interest rate period is over, there is no more payment assistance

- if thoughts of refinance do not materialize or income does not increase one could struggle the absence of payment assistance

Get trusted advice from a local expert that some call the best mortgage guys in Raleigh, NC. The Martini Mortgage Group offers local home loan programs such as Conventional Loans, FHA Loans, Jumbo Loans and USDA Loans to name a few. To contact loan officer Logan Martini or loan officer Kevin Martini for a financial review simply call (919)238-4934 or stop by the office since the Martini Mortgage Group is local and is located in downtown Raleigh, NC at 507 N Blount St, Raleigh, NC 27604.

Martini Mortgage Group Buydown Loan Program Can Be Combined with the Martini Mortgage Group ‘No Contract Lock’

The No Contract Lock (a.k.a. Lock & Shop) is where a clients can lock a loan program for a Conventional Loan, FHA Loan or VA loan for up to 90-days at no charge with a FREE float down option.

Future homeowners can shop for their next home worry-free in Raleigh, NC knowing their interest rate is protected for 90-days. For added purchase worry-free protection, if the interest rate rises their loan rate is protected. Plus, if the loan program interest rate drops, as a mortgage lender, we offer a free float-down option. This is a lending industry first.

Logan Martini | Raleigh Mortgage Broker with Martini Mortgage Group

There are many lenders in Raleigh but many believe the best mortgage company in the industry is the Martini Mortgage Group

See our online reviews on the service we offer and why a top rated in the lending programs and services we offer but also many believe we are the best mortgage company in Raleigh, North Carolina.