Navigating the world of home loans can be a daunting task. For those who find the conventional loan a tough road, the Federal Housing Administration (FHA) offers an alternative: the FHA home loan. This mortgage assists borrowers with lower credit scores and/or minimal down payments; the FHA loan has made homeownership attainable for countless first-time and repeat homebuyers. But what is it, exactly, and how does it differ from a conventional loan? Entrust the Martini Mortgage Group to clarify the complexities and accompany you throughout the journey.

What Exactly is an FHA Home Loan?

An FHA home loan is a mortgage insured by the Federal Housing Administration. Unlike conventional home loans, which the federal government does not insure, FHA loans are backed by the U.S. government. This government backing means lenders are more willing to approve loans for individuals who might not qualify for conventional loans.

If a borrower defaults on an FHA loan, the FHA will cover the loss, thus minimizing the risk for lenders. Established in the 1930s during the Great Depression, the FHA loan program was created to stimulate the housing market by making loans more accessible and affordable for people with poor credit or limited savings.

Crucial Components of an FHA Home Loan:

- Lower Down Payment: One of the most appealing aspects of an FHA loan is the low down payment requirement. Borrowers can put down as little as 3.5% of the home’s purchase price, making it easier for many to step into homeownership.

- Flexible Credit Score Requirements: FHA loans are known for their lenient credit requirements. While a conventional loan might demand a higher credit score, an FHA loan might be available to those with scores as low as 500. However, better terms are usually given to those with scores above 580.

- Mortgage Insurance: FHA loans come with mandatory mortgage insurance premiums (MIP) due to the lower down payment and lenient credit requirements. This insurance protects the lender if the borrower defaults. There’s an upfront MIP, a one-time charge, and an annual MIP, split into monthly payments.

- Loan Limits: FHA loans have limits, which vary by region and are based on local median home values. This ensures that they cater mainly to those purchasing moderately priced homes.

- Property Requirements: Homes purchased with an FHA loan must meet specific safety, security, and soundness requirements. This might require the borrower to make necessary repairs before the loan gets approved.

- Owner-Occupied Restriction: FHA loans are intended for primary residences only. Borrowers cannot use an FHA loan to purchase a vacation home or investment property.

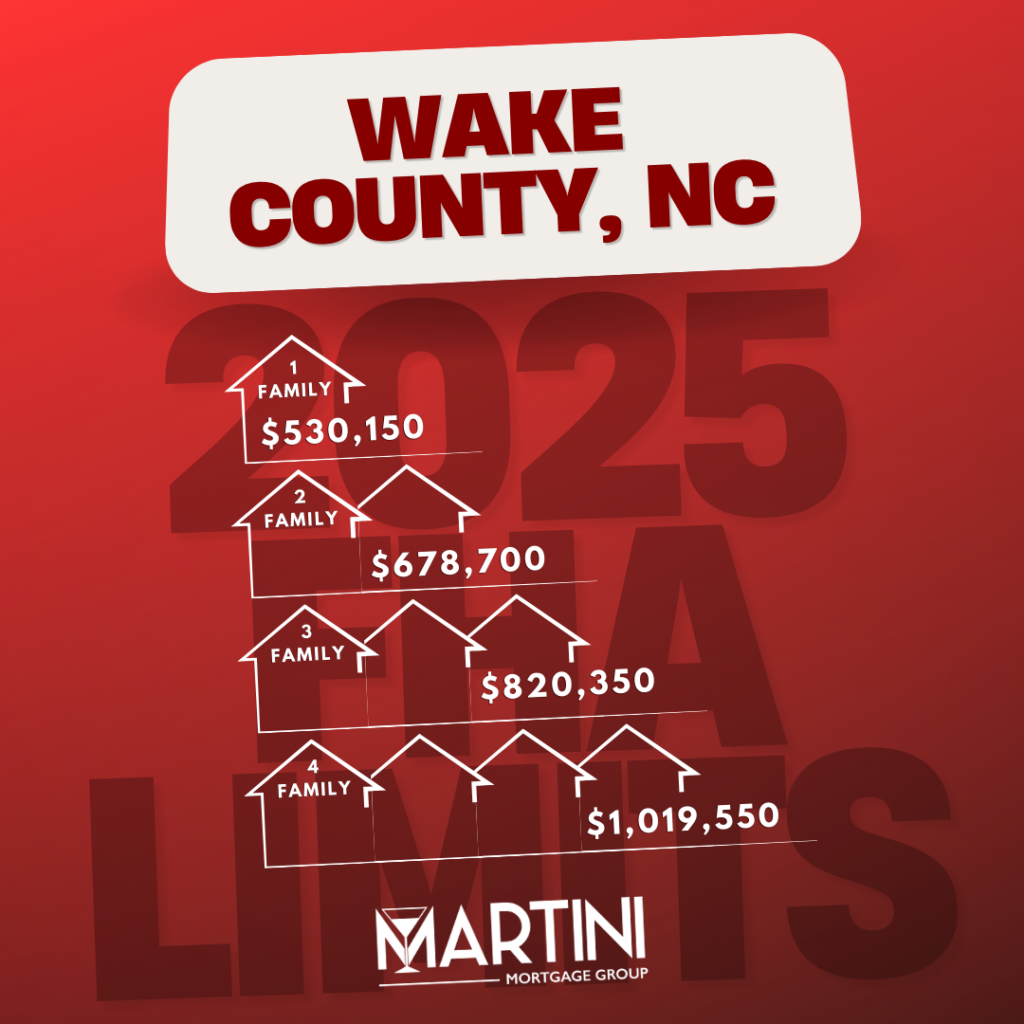

2025 FHA Mortgage Limits for Wake County, NC (Raleigh – Cary Metropolitan Statistical Areas)

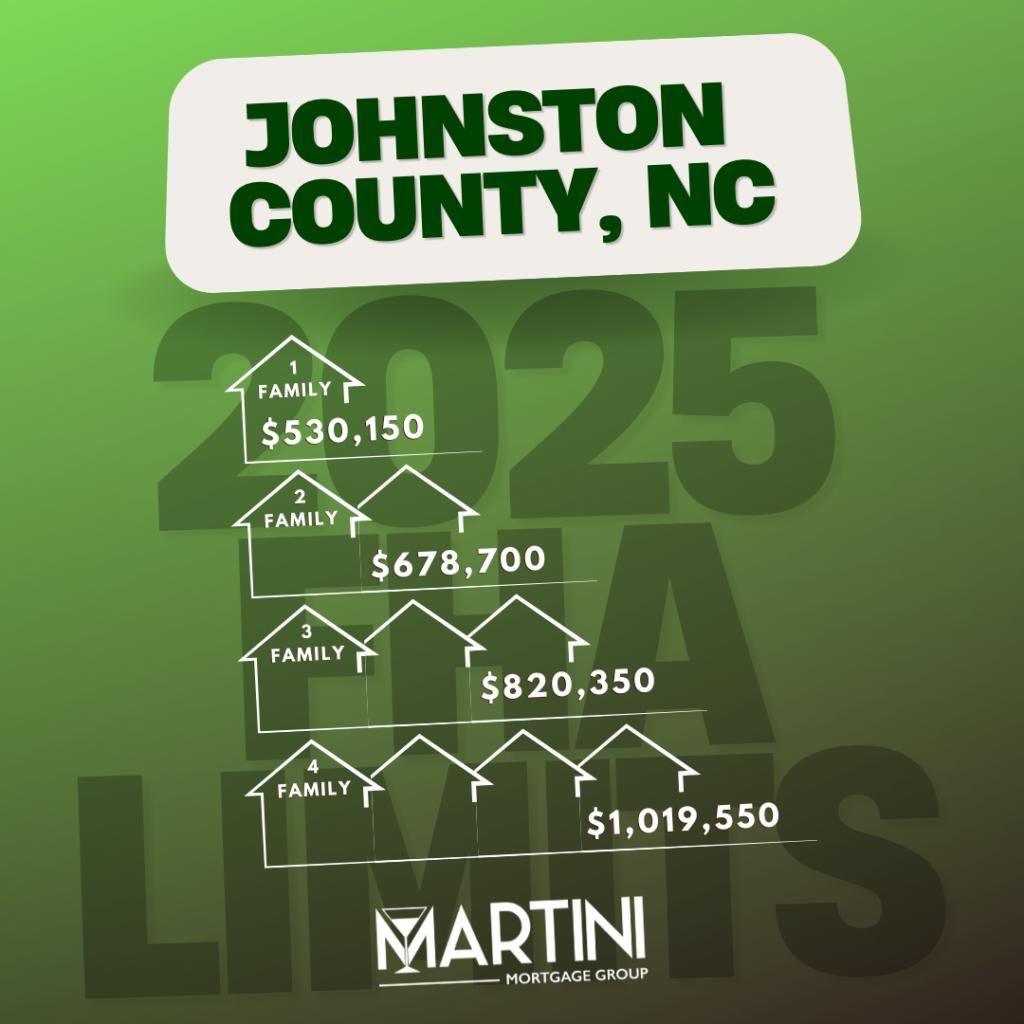

2025 FHA Mortgage Limits for Johnston County, NC (Raleigh – Cary Metropolitan Statistical Areas)

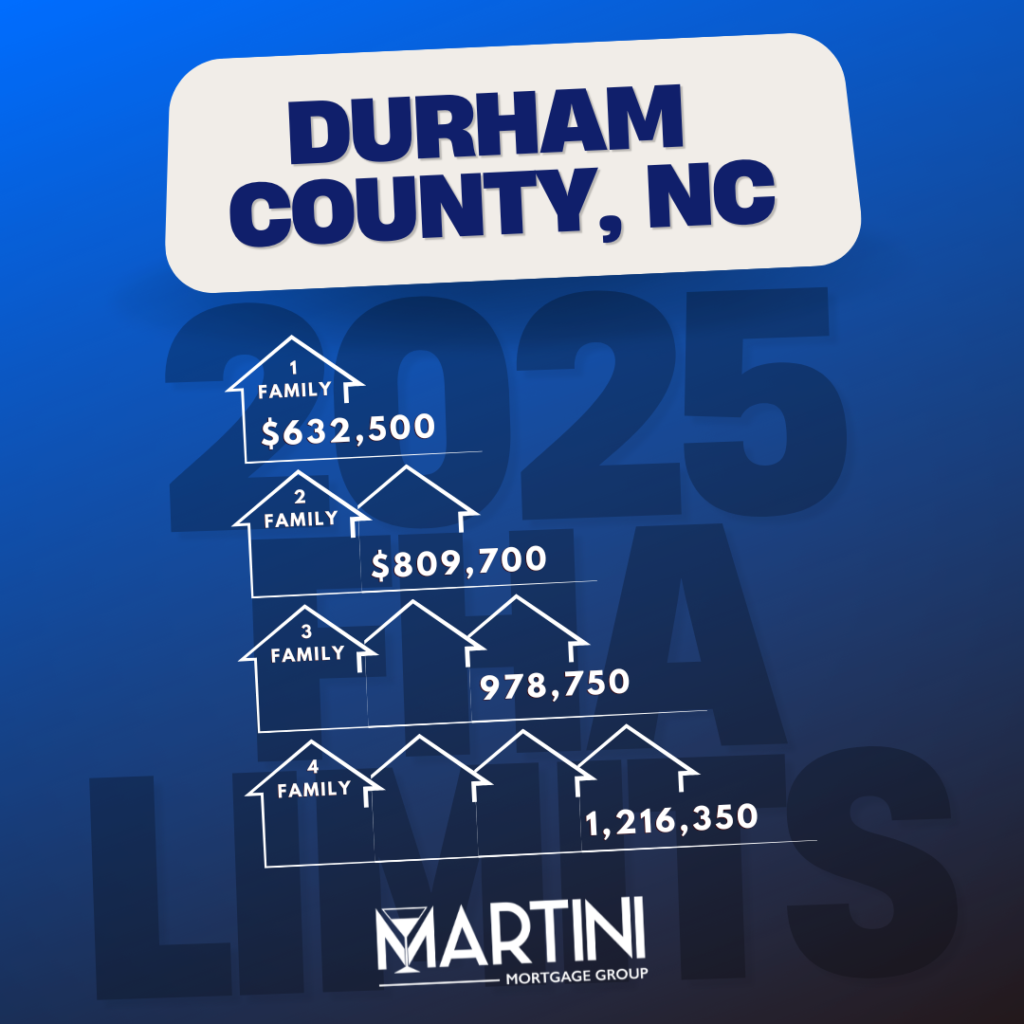

2025 FHA Mortgage Limits for Durham County, NC (Durham – Chapel Hill, NC Metropolitan Statistical Areas)

In Conclusion, by Martini Mortgage Group

The FHA home loan serves as a lifeline for many aspiring homeowners. Its lenient requirements and government backing offer a path to homeownership that might otherwise remain blocked. However, it’s essential to understand its components, from mortgage insurance to property requirements, to determine if it’s the right choice for your financial and homeownership goals. Like any significant financial decision, consultation with a Mortgage Strategist with the Martini Mortgage Group will offer personalized insights and advice. Contact the Martini Mortgage Group at (919) 238-4934 and book your complimentary consultation today.

The Martini Mortgage Group isn’t merely a Raleigh Mortgage Broker in Raleigh, North Carolina. Their reach spans across all 100 counties in North Carolina. It extends into Florida, Georgia, Indiana, South Carolina, and Virginia, serving individuals and families alike.