In the universe of home-buying, knowledge is power. As you embark on one of life’s most exciting journeys, understanding your financing options is crucial. One term you’ll frequently encounter is the “conventional loan.” But what is it? How does it work? And how does it stack up against other mortgage options? The Martini Mortgage Group is here to unravel the mysteries and guide you through every step.

What Exactly Is a Conventional Loan?

Imagine navigating a vast sea of mortgage loans. Among the many, the conventional loan stands out. A government entity neither insures it nor is it a government loan. Consider it the all-rounder of the mortgage world, versatile and widely accepted.

Most conventional loans fall under the “conforming” category, meaning they adhere to the guidelines set by government-sponsored enterprises like Fannie Mae and Freddie Mac. These entities play a pivotal role in the U.S. housing market by purchasing mortgages from lenders and selling them to investors. This cycle ensures a continuous flow of funds, making homeownership accessible to many.

While conventional loans come in various term lengths, the 15-year and 30-year options reign supreme among borrowers.

The Crucial Components of Conventional Loans

Here is the Martini Mortgage Group breakdown of what you need to qualify for a conventional loan:

- Down Payment: Think of this as your initial investment. For first-time homebuyers, you can enter the market with as little as a 3% down payment. However, this percentage varies based on your profile and the property type. For instance, non-first-time buyers or those with higher incomes might require a 5% down payment, while a second home could command a 10% upfront payment.

- Private Mortgage Insurance (PMI): If your down payment is less than 20%, you’ll encounter PMI. It’s a safety net for lenders in case of loan defaults. PMI costs fluctuate based on your credit score, loan type, and down payment size. But fear not! PMI isn’t eternal. Once you hit 20% equity in your home, a simple request can be removed from your payments.

- Credit Score: A credit score, typically above 620, is the golden ticket to a conventional loan. This three-digit number is a reflection of your financial behavior and reliability.

- Debt-to-Income Ratio (DTI): This percentage is the relationship between your monthly debt obligations and your gross monthly income. While approvals can stretch up to 50% DTI, a lower DTI amplifies your chances.

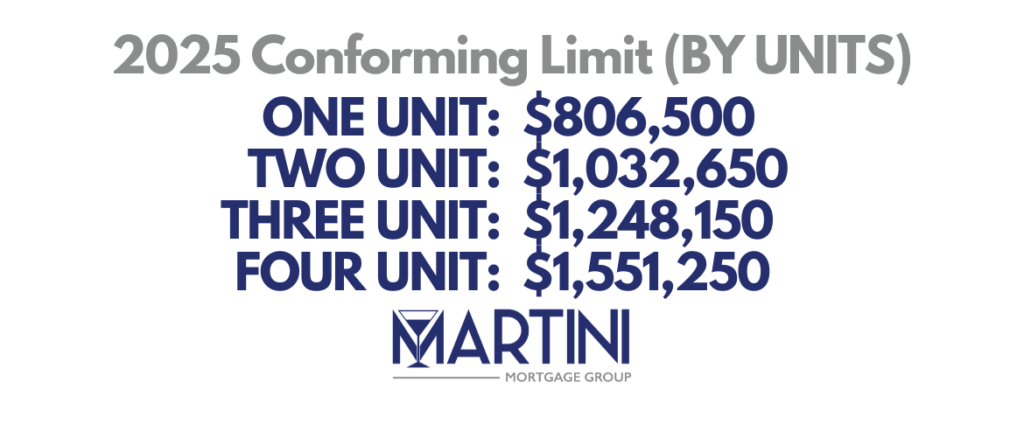

- Loan Size: To qualify as a conforming conventional loan, your loan amount should be within limits set by Fannie Mae and Freddie Mac. For 2024, the benchmark for a single-family home is $766,550, except in high-cost regions.

RESOURCE ON CONFORMING LOAN LIMITS FOR 2025 SEE: Martini Mortgage Group: 2025 Conforming Loan Limits See a Boost—Here’s What You Need to Know

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Today's Mortgage RatesThe Conventional Loan Showdown: How Does It Compare?

Conventional vs. VA Loans

VA loans are reserved for veterans, active-duty Servicemembers, and their surviving spouses. Unlike conventional loans, VA loans require no down payment and skip mortgage insurance. However, they have occupancy restrictions and may have a variable VA funding fee.

Conventional vs. FHA Loans

While both loans cater to different credit score brackets, the main distinction lies in mortgage insurance. FHA loans have lifelong mortgage insurance. Conversely, conventional loans can dismiss mortgage insurance once certain conditions are met.

Conventional vs. USDA Loans

USDA loans target rural areas and come with specific income limits. Unlike conventional loans that don’t cap income, USDA loans consider household earnings. While PMI isn’t a concern for USDA loan borrowers, a guarantee fee is applicable, often more affordable than PMI.

In Conclusion by, Martini Mortgage Group

Stepping onto the cusp of homeownership, a conventional loan often emerges as the golden key to your dream abode. Renowned for its flexibility and broad approval, it remains a top pick for many. However, the mortgage landscape is intricate and diverse. The perfect choice marries your needs, fiscal well-being, and future goals. This is where the Martini Mortgage Group shines—guiding you with unparalleled expertise and unwavering dedication. Embark on a home-buying voyage that’s both successful and enlightening. Dive into a realm where knowledge powers every decision, leading you to the doorstep of your dream home. Ready to navigate this journey with us? Contact the Martini Mortgage Group at (919) 238-4934 and book your complimentary consultation today.

The Martini Mortgage Group is more than just a Raleigh mortgage broker based in Raleigh, North Carolina. They extend their services to individuals and families across all 100 counties of North Carolina and in Florida, Georgia, Indiana, South Carolina, and Virginia.

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Today's Mortgage Rates